Recent market turmoil has given the Financial Stability Board (FSB) “all the more reason” to develop a globally consistent regulatory framework, an official said on Thursday, Coindesk reports.

The international body monitors and recommends standards for the global financial system, and is made up of major economies and institutions like the International Monetary Fund (IMF).

Steven Maijoor, chair of the Financial Stability Board’s crypto working group, said:

Rapid growth of crypto markets in the presence of structural vulnerabilities and incomplete regulations and supervision means that they will soon reach a point where they represent a threat to the stability of the global financial system

The international body monitors and recommends standards for the global financial system, and is made up of major economies and institutions like the International Monetary Fund (IMF).

Read full article on Coindesk.

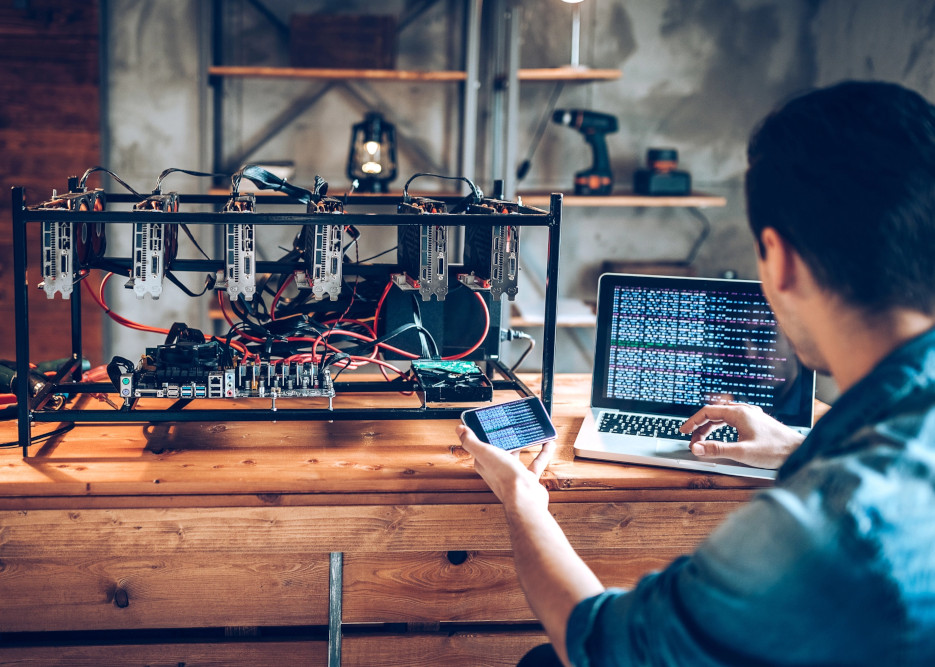

22 year old Ahmad Abu Daher, based in Lebanon, and his team of more than 40 Lebanese and Syrian employees, earn $20,000 by working around the clock to man thousands of Bitcoin mining machines across the country, CNBC reports.

“We can’t sleep. We can’t have any break,” Abu Daher told CNBC. “All of my team are still awake. They don’t sleep. Our shift is working 16 hours per day, and sometimes, up to 18 or 19 hours.”

According to CNBC, the local currency has lost more than 95% of its value since 2019, the minimum wage has plunged to $17 a month, pensions are virtually worthless, and bank account balances are just numbers on paper. Banks close without warning and ATMs are often either out of cash or entirely offline from nationwide blackouts. When locals are able to gain access to their accounts, many tell CNBC that they have grown accustomed to withdrawing money at 15% of its original worth.

Against this backdrop, Abu Daher jumped into the crypto mining business a little over two years ago. He and a friend began with three machines running on hydroelectric power in Zaarouriyeh, a town 30 miles south of Beirut in the Chouf Mountains.

“When we started, it was our great idea to make money while sleeping or eating,” said Abu Daher. Nowadays, Abu Daher says he is online 20 hours a day.

Binance CEO Changpeng “CZ” Zhao has strongly advised cash-strapped and inexperienced investors to stay away from trading cryptocurrencies amid extreme market volatility and unpredictability, Cointelegraph reports.

On a Nov. 14 Zhao-led “Ask Me Anything” Twitter space hosted by Binance the CEO suggested that unsophisticated investors wait out the turbulent period instead of risking money needed for living expenses:

You should not invest in crypto if you're using money that you need for next week or next month, you should only be using discretionary cash that you don't need for a long time, like maybe a couple of years.

For those who do have that spare cash, Zhao advised inexperienced investors and traders to think twice before deploying capital into the market in the near future.

Crypto giant Binance signed a nonbinding agreement on Tuesday to buy FTX's non-U.S. unit to help cover a "liquidity crunch" at the rival exchange, in a stunning bailout that raised fresh concerns among investors about cryptocurrencies, Reuters reports.

The deal between high-profile rivals Sam Bankman-Fried, FTX's CEO, and Binance CEO Changpeng Zhao came as speculation about FTX's financial health snowballed into $6 billion of withdrawals in the 72 hours before Tuesday morning.

The pressure on FTX came in part from Zhao, who had tweeted on Sunday that Binance would liquidate its holdings of the rival's token due to unspecified "recent revelations."

The move, a dramatic reversal in fortunes of billionaire Bankman-Fried, 30, is the latest emergency rescue in the world of cryptocurrencies this year, as investors pulled out from riskier assets amid rising interest rates. The cryptocurrency market has fallen by about two-thirds from its peak to $1.07 trillion.

Crypto exchange FTX saw around $6 billion of withdrawals in the 72 hours before Tuesday morning, according to a message to staff sent by its CEO Sam Bankman-Fried that was seen by Reuters.

In a surprise move, Changpeng Zhao, boss of major rival Binance, said on Tuesday the company signed a nonbinding agreement to buy FTX's non-U.S. unit, FTX.com, to help cover a "liquidity crunch" at FTX.

"On an average day, we have tens of millions of dollars of net in/outflows. Things were mostly average until this weekend, a few days ago," Bankman-Fried wrote in a message to staff sent on Tuesday morning.

"In the last 72 hours, we've had roughly $6b of net withdrawals from FTX," he wrote, adding that withdrawals at FTX's main unit, FTX.com, are "effectively paused," an issue that would be resolved in "the near future."

"Most of the details (of the deal) still aren't hashed out," he wrote, adding that he did not have a "definitive answer" for questions including "what exactly is the transaction" and "what entities would it include."

FTX did not immediately respond to a request for comment.

Bitcoin and Ether fell in Thursday morning trading in Asia along with all other top 10 cryptocurrencies by market capitalization, excluding stablecoins, as the U.S. Federal Reserve announced a fourth consecutive rate hike of 75 basis points on Wednesday, Forkast reports.

Leading memecoins Dogecoin and Shiba Inu token saw the heaviest losses after several days of significant gains following Elon Musk’s purchase of social media platform Twitter Inc.

Bitcoin fell 1.5% to US$20,147 in the 24 hours to 8 a.m. in Hong Kong, while Ether fell 3.8% to US$1,517, according to data from CoinMarketCap. Solana saw significant losses, falling 4.8% to US$30.71, while Cardano dropped 4% to US$0.38.

Shiba Inu token fell 7.8% to US$0.00001176, though was still trading up 8.8% over the past seven days, while Dogecoin fell 9.4% to US$0.12, though it was still up over 70% in the past week. Since purchasing Twitter, Elon Musk has tweeted pictures of shiba inu dogs — the breed of dog the Doge meme is based on — and has floated the idea of integrating Dogecoin as a payment method on the platform.